As Your Business Grows

We Deliver The FUNDS

We Deliver The FUNDS

.jpg)

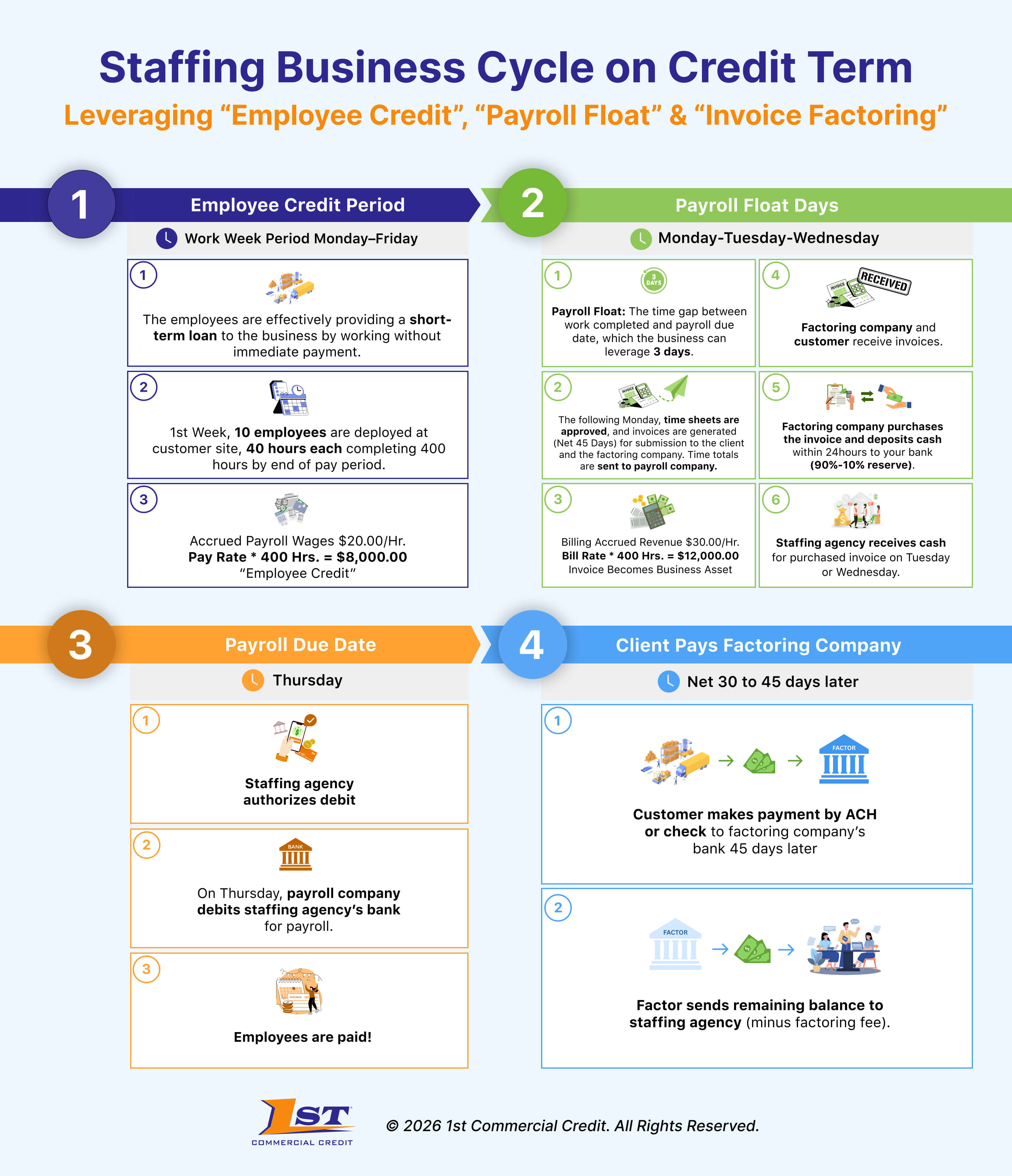

Staffing companies face a unique cash flow challenge: they must pay employees weekly or bi-weekly, while clients often take 30, 60, or even 90 days to pay invoices.

This gap between payroll and receivables creates constant pressure on cash flow, especially during periods of rapid growth.

To solve this, many staffing agencies turn to two main financing options: invoice factoring and a bank line of credit. While both provide access to working capital, they operate very differently and serve different business needs.

Unlike most industries, staffing companies must front payroll before receiving payment from clients. Without reliable cash flow, staffing companies risk missing payroll, turning down contracts, or limiting growth.

Common challenges include:

1) You can target clients your competitors are selling to on credit terms, as offering net 30, 60, or 90-day terms is no longer an issue.

2) Prepares your business for growth

3) Your business will have more opportunities to grow:

Leveraging “Employee Credit”, “Payroll Float” & “Invoice Factoring”

Invoice factoring is a financing solution where a staffing company sells its unpaid invoices to a factoring company in exchange for immediate cash. Instead of waiting weeks or months to get paid, you receive funds upfront, often within 24 hours. Factoring is based primarily on the creditworthiness of your clients, not your business financials.

A bank line of credit is a revolving loan that allows staffing companies to borrow against their receivables. The bank evaluates your financials, credit history, and overall risk before approving funding. You can draw funds as needed and repay them over time. Unlike factoring, this is debt that must be repaid, often with strict terms and covenants.

.jpg)

A Factoring Company purchases invoices at a discount and charges a “Discount Fee”, simultaneously transferring cash to the staffing agency in exchange for the Invoice Asset.

Invoice Factoring is not a loan and fees are not calculated with interest, there is no debt, and there are no installment payments like a loan.

It is similar to offering a client a 2% or 3% discount for early payment or accepting a credit card payment from a client with a 2.5% fee deduction for the service. The business receives a discounted amount.

What happens when a staffing company lands large contracts but has to wait over 60 days to get paid?

In this case, a healthcare staffing agency we worked with faced exactly this challenge, and found a way to turn delayed payments into immediate cash flow.

Discover the full story: Read Full Story

Invoice factoring is ideal when:

A bank line of credit may be better if:

For most staffing companies, especially those in growth mode, invoice factoring is the more practical solution.

It provides fast, flexible access to cash, aligns with your revenue cycle, and removes the burden of waiting for client payments.

A bank line of credit can be useful for well-established firms, but it often lacks the speed and flexibility required in the staffing industry.

Factoring is often better for staffing companies that need fast cash flow and flexible funding, especially during growth phases.

With invoice factoring, funding can happen within 24 to 72 hours.

Yes, but approval depends on strong financials, credit history, and meeting strict banking requirements.

Because staffing companies must meet payroll before getting paid, factoring helps bridge that gap quickly and efficiently.

Stop waiting 30-90 days for your customers to pay their invoices. Factor with 1st Commercial Credit and receive the working capital your business needs to grow.

.png)

.png "Read More About Factoring Staffing Agencies")

.jpg "Read More About Factoring Freight Trucking Companies")

.jpg "Read More About Factoring Staffing Agencies")

.jpg "Read More About Factoring Staffing Agencies")

.jpg "Read More About Factoring Freight Trucking Companies")