As Your Business Grows

We Deliver The FUNDS

We Deliver The FUNDS

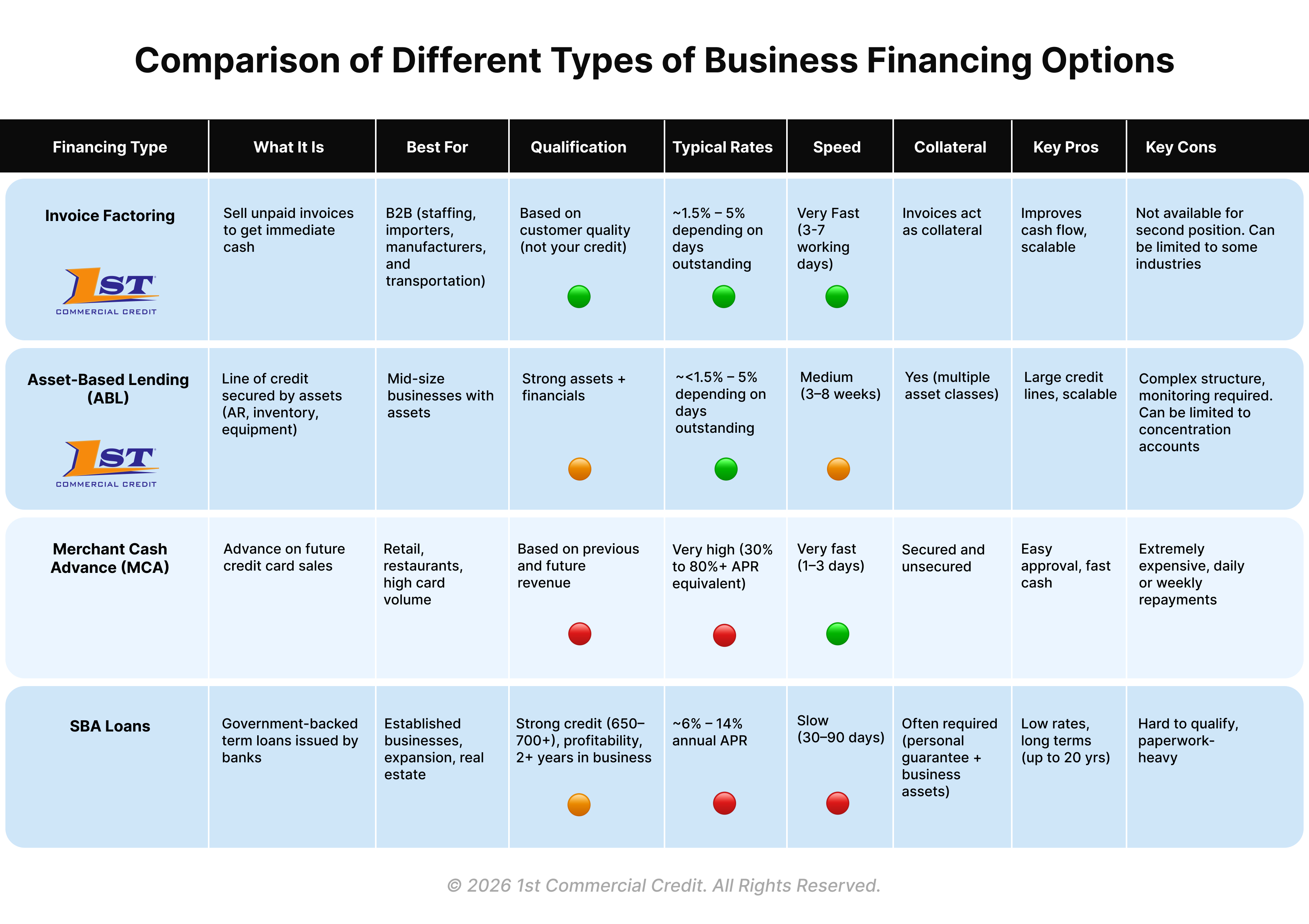

Choosing the right business financing option can have a significant impact on your company’s growth, cash flow, and long-term stability. Whether you’re looking to cover short-term expenses, invest in equipment, or scale operations, understanding how each financing option works is crucial.

With so many options available in the U.S., from traditional loans to alternative funding solutions, it can be difficult to determine which one best fits your business. Each type of financing comes with its own qualification requirements, costs, repayment structures, and timelines.

This guide breaks down the most common business financing options, how they work, and how they compare so that you can make a more informed decision.

.jpg)

Most business financing options fall into three main categories:

The key difference between these categories lies in how lenders evaluate risk. Some focus on your credit and financial history, while others look at your revenue, customers, or assets.

Invoice factoring allows businesses to convert unpaid invoices into immediate cash. Instead of waiting 30, 60, or even 90 days for payment, you receive a large portion of the invoice value upfront.

.jpg)

At 1st Commercial Credit, invoice factoring is designed to support businesses that rely on consistent cash flow to operate and grow. Invoice factoring is commonly used in industries like staffing, importers, manufacturers, and transportation.

→ Learn About Our Invoice Factoring Program

Asset-Based Lending (ABL) provides a revolving line of credit secured by business assets such as receivables, inventory, or equipment.

.jpg)

At 1st Commercial Credit, ABL is used to provide ongoing access to working capital for growing businesses. This financing option is often a strong fit for mid-sized businesses with a solid asset base.

→ Learn about our Asset-Based-Lending program

A Merchant Cash Advance provides a lump sum of capital in exchange for a percentage of future sales. Repayments are typically made daily or weekly based on revenue.

MCAs are typically used when other financing options are unavailable, due to their higher cost and repayment terms.

SBA loans are government-backed loans issued by banks and other lenders. Because a portion of the loan is guaranteed, lenders are able to offer lower interest rates and longer repayment terms.

SBA loans can be a strong option for established businesses. However, they are often difficult to access for companies that need fast funding or have cash flow challenges.

These are the most common SBA loans, offering qualified U.S. businesses access to relatively low-interest financing through approved lending partners. Loan amounts can go up to $5 million, and funds can be used for a wide range of purposes, including working capital, equipment purchases, real estate, or refinancing existing debt.

One of the main advantages of SBA 7(a) loans is their flexibility. They are designed to support small businesses that may have struggled to secure traditional financing, while still offering competitive rates and longer repayment terms. However, qualification requirements remain strict, and borrowers typically need strong credit and solid financials. For businesses planning a major investment or expansion, this program can be a viable option, provided they can navigate the approval process.

SBA 504 loans are specifically designed for financing major fixed assets, such as commercial real estate or large equipment purchases. These loans are structured differently than other SBA programs, typically involving three parties: a private lender, a Certified Development Company (CDC), and the borrower, who provides a down payment.

This structure allows businesses to access long-term, fixed-rate financing with relatively low interest rates. Because of their stability and predictability, SBA 504 loans are often used by companies planning significant expansion projects. However, they are limited to specific use cases and are not intended for general working capital needs.

SBA Express loans are a streamlined version of the 7(a) program, designed to provide faster decisions and reduced processing times. Loan amounts are smaller, up to $500,000, but approval decisions can often be made within a few days instead of several weeks.

While the application process is faster, funding may still take additional time to be disbursed. Interest rates can also be slightly higher compared to standard SBA 7(a) loans, reflecting the reduced turnaround time. This option may appeal to businesses that need quicker access to capital but still want to stay within the SBA framework.

SBA Microloans are smaller loans, with a maximum amount of $50,000, typically offered through nonprofit intermediary lenders. These loans are often used for working capital, inventory, or smaller operational expenses.

Microloans tend to be more accessible than other SBA programs and may be available to newer businesses or those with less established credit. In addition to funding, many programs offer technical assistance and business support, which can be valuable for early-stage companies. While the loan amounts are limited, they can serve as a stepping stone for businesses looking to build financial stability.

When comparing financing options, it’s helpful to look at a few key factors:

Many businesses operate in environments where waiting weeks or months for funding is not practical. Delayed customer payments, rapid growth, or seasonal demand can all create cash flow gaps.

Alternative financing solutions, such as invoice factoring and asset-based lending, are designed to address these challenges by aligning funding with real business activity, rather than relying solely on credit scores or historical performance.

1st Commercial Credit focuses on financing solutions that are flexible, scalable, and aligned with how businesses actually operate.

These include:

Rates for factoring and ABL start as low as 1.5%, making these solutions competitive while still providing fast access to capital.

It’s important to note that 1st Commercial Credit does not offer SBA loans or Merchant Cash Advances. Instead, the focus is on financing options that support sustainable growth and cash flow management.

1st Commercial Credit is recognized as one of the largest independent providers of asset-based financial services for small to mid-sized businesses and offers funding as little as $10,000 a month to $10 million in credit line facilities.

→ Learn More About Our Company

The best financing option depends on your business needs and situation. Consider:

Business financing is not just about accessing capital. It’s about choosing a structure that supports your operations and growth over time. While traditional loans can offer lower rates, they may not provide the flexibility many businesses need. On the other hand, higher-cost options like MCAs can create additional financial pressure.

Solutions such as invoice factoring and asset-based lending offer a more flexible approach, helping businesses maintain cash flow, invest in growth, and adapt to changing demands. Understanding how these options work, and when to use them, can help you make more informed financial decisions and position your business for long-term success.

Stop waiting 30-90 days for your customers to pay their invoices. Factor with 1st Commercial Credit and receive the working capital your business needs to grow.

.png)

.png "Read More About Factoring Staffing Agencies")

.jpg "Read More About Factoring Freight Trucking Companies")

.jpg "Read More About Factoring Staffing Agencies")

.jpg "Read More About Factoring Staffing Agencies")

.jpg "Read More About Factoring Freight Trucking Companies")